How Financial Statements Are Used in Business Decision-Making

Financial statements reside humbly in the background of most organizations. Rubbed through each month, filed away, and occasionally read. On the other hand, when decisions become uncertain, such as growth strategies, cost management, staffing, and price levels, these documents assume greater importance.

From an overall standpoint, financial statements are not decision makers. Sometimes, they are considered context. They influence how business owners, entrepreneurs, and corporate finance professionals see what is really happening, and what might happen in the near future. This article is a discussion on the role that financial statements play in the decision-making process, not as a prescription, but as a way to help think more clearly.

What Financial Statements Represent in Practice

On a fundamental level, financial statements bring organization to business activity. They convert operational motion into something quantifiable: revenue earned, costs incurred, assets built, obligations created.

In practice, businesses rely on three core statements. Most businesspeople think of these without having a mental division between statements. The income statement, the balance sheet, and the cash flow statement each have a different role in determining performance and position.

Taken together, they allow the decision maker to step back from day-to-day operations and view the business as a whole. Here, the role of financial statements in business becomes less a question of reporting but one of interpretation. Numbers alone rarely explain why something is happening. But they do highlight where attention may be needed.

Financial Statements as a Decision Context, Not a Verdict

One misconception about financial statements is that they indicate the course of action the business should take. They don’t. What they provide is a shared frame of reference.

For instance, when the conversation revolves around whether the profit margins are getting thinner, the income statement becomes an integral part of the conversation. Thus, when cash flow is an issue despite the existence of profit, the cash flow statement business decisions come to the fore. Similarly, when there are questions of risk, the balance sheet analysis of business decisions becomes an important area to look at.

Financial statements, when utilized effectively for business decisions, operate best when viewed as the start of a conversation, where they are used to establish some trade-offs, constraints, assumptions, but cease to define any action.

How Managers Commonly Use Financial Reports

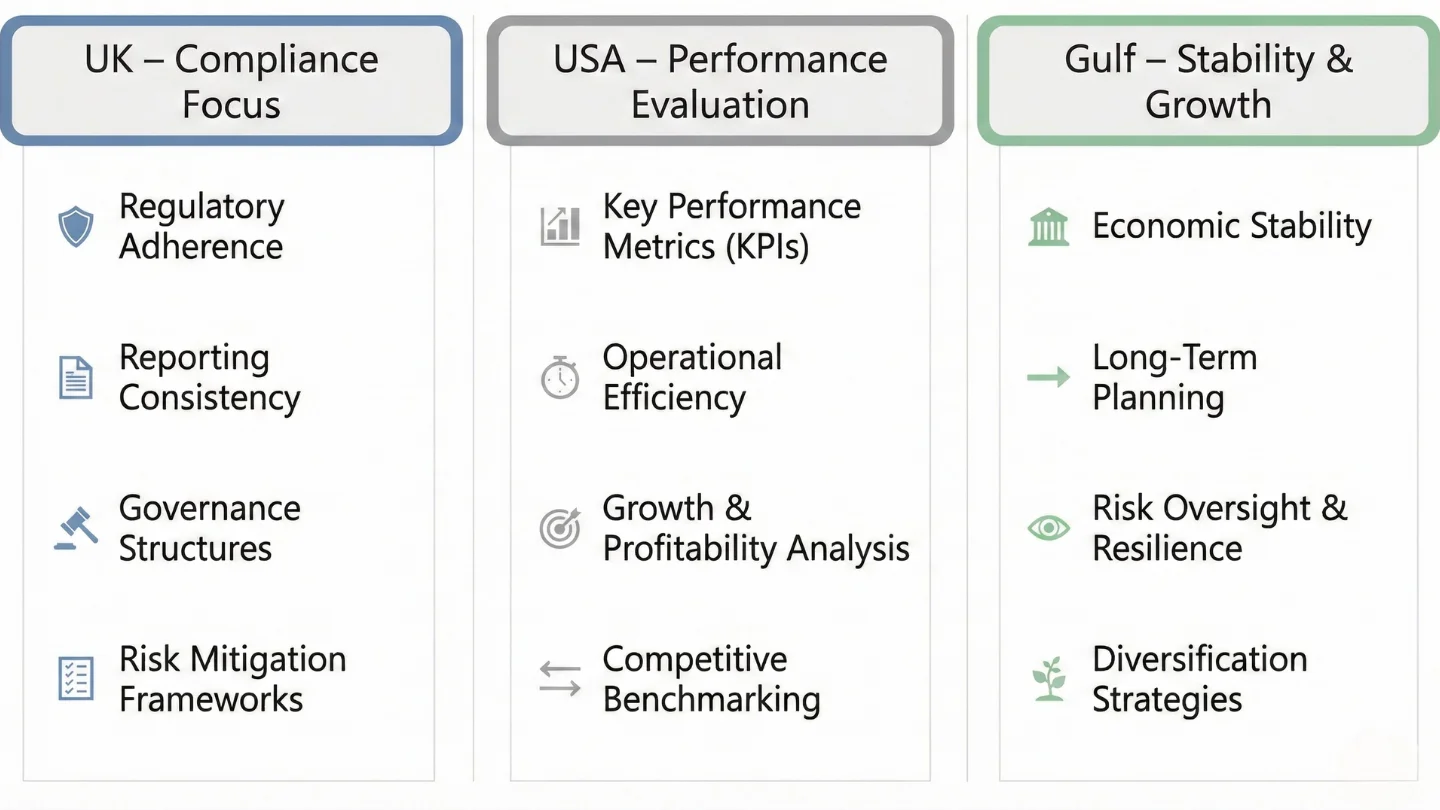

Similarly, regardless of regions and terms of reference, managers find common uses for financial statements.

In the case of the UK, management accounts, as well as its relationship with management decisions, might often go hand in hand. This is because regular reporting allows managers to compare actual results with planned ones, following which they adjust their focus. Emphasis is usually given to consistency, control, and compliance-based reports.

In the USA, due to financial statement analysis for decision-making purposes, there is more emphasis placed upon performance evaluation. The emphasis placed upon financial statements for decision-making purposes can be a means for the leadership to determine if their business model is working as it should or not.

There is a stabilizing force associated with financial reporting, particularly for business owners within Gulf markets. The presence of statements is utilized to maintain oversight, minimize risks, and enhance planning, based on an environment that is conducive to rapid growth and steadily tightening regulations. Business financial reporting prioritizes decision-making that is visible and quite discipline-driven.

Nevertheless, the fundamental goal behind such regional variations remains the same, and it is the reduction of uncertainty.

Income Statements and Operational Judgement

Income statement-based decision making is often the most accessible place to start. “Revenue,” “expenses,” “profit,” these concepts are all quite intuitive.

Businesses frequently refer to an income statement when making decisions about:

- Cost structure changes

- Pricing Effectiveness

- Departmental performance

- Sustainability of the current operations

Still, the income statement is also a potentially misleading document when viewed in isolation, and the smoothing of accrual accounting over time obscures variances, either creating pressures or overstating stability, which is why experienced decision-makers review the income statement with other reports, but never in isolation.

Balance Sheets and Business Stability

Analysis of balance sheet data in making business decisions is less intuitive, yet perhaps more revealing.

Assets, liabilities, and equity can provide useful information in terms of how the business is financed or even its ability to sustain adversity. Debts, working capital, or long-term indebtedness may also originate from here. Financial ratios for management decision-making purposes, e.g., liquidity or solvency ratios, may be based on the balance sheets of an enterprise. In growing firms, balance sheets may indicate strain before it becomes operationally apparent. Investment build-ups, receivables issues, and rising short-term debt may not disrupt normal operations now, but they threaten future choices.

Cash Flow Statements and Reality Checks

There are few financial statements as likely to confront assumptions as the cash flow statement.

Profitable, yet not able to make ends meet, a business can be. The cash flow statement can influence a number of business decisions, especially in situations involving business expansions, investments, and uncertainty. The decision to make hires, invest in purchases, and make business commitments can be affected, not necessarily the profits. This is also where budgeting and forecasting decisions start to feel grounded. “Historical patterns of cash flow … inform our expectations, but also underscore volatility.” This statement is where many owners see a description of success that makes sense to them.

Financial Statements in Planning and Forecasting

Financial statements are retrospective by their very nature, but prospective planning is heavily influenced by them. Business organizations often start with historical financial performance evaluations as a precursor to forecasts. Patterns are seen, cycles are observed, and the behavior of costs becomes clearer and more predictable over time, although it may not be a direct part of the forecast briefs. When it comes to the interpretation of financial statements in the context of business planning, restraint is advised. This is because past performance does not guarantee future performance. However, it has been found that ignoring the data only increases the risk.

Common Challenges and Misinterpretations

Although it has much merit, it is often misunderstood.

Some businesses may be depending too much on minor figures or information without context, and there is also the possibility of delaying certain reviews until the issue becomes apparent, aside from concentrating on one piece of information and leaving others behind. Another issue is that of overconfidence. This is because it is possible that familiarity breeds only confidence, but it is not necessarily linked to expertise. The figures might be interpreted differently based on different conditions. That why it is recommended to always consider a reputed financial consultant

Where Bookkeeping Connects to Decision Quality

“Accurate bookkeeping is often ignored at times when everything is functioning as expected. However, anyone can see its significance in uncertain times.”

Bookkeeping is the foundation of financial reporting. Without consistency, clarity, and a clear understanding, financial reports lose reliability. Decisions made from imperfect and misconstrued information create a form of risk that is avoidable. In an advisory context, bookkeeping makes a contribution to decision-making indirectly: it assists in ensuring financial information closely represents the actual world. It removes noise. It means the conversation can focus on interpretation rather than correction. This connection is subtle, but critical.

Final Thoughts

Financial statements are no substitute for judgment. They are a guide to it.

When used properly, these methods assist companies in slowing down, looking at the situation, and making better decisions. However, misusing these methods can result in a reinforcement of what the company assumes, rather than challenging the assumptions. The use of financial statements in decision making in business can be understood from the perspectives that are not so technical.

Clarity, consistency, and context are more important than complexity.

To understand how structured financial reporting supports clearer financial discussions, explore our bookkeeping advisory approach or start a conversation with IQ Insight Consulting.