How Businesses Typically Approach Tax Planning

Tax planning is something that most companies understand to be an important issue, but one that is rarely tackled with complete clarity. Tax planning is an issue that can be found at the crossroads of financial management, regulatory compliance, and business strategy. Tax planning is something that is often considered to be complex, but it is, in fact, more about perspective than it is about strategy.

For companies that are growing, tax planning is not, as it is often considered to be, about minimizing tax liabilities. Instead, it is about realizing the impact of business decisions, financial reporting, and business structure on tax liabilities. Tax planning is something that, as companies grow, is more and more aligned with cash flow, corporate governance, and financial discipline.

Learning about tax planning is an effective way to gain an understanding of the development of financial discipline.

What Business Tax Planning Usually Means in Practice

“Tax planning?” and one thinks of complicated structures or schemes. Most businesses, however, carry out tax planning in much more straightforward and down-to-earth ways.

Fundamentally, business tax planning is a question of anticipation. Businesses seek to forecast how their present activities, such as pricing, expansion, and employment, may have future implications for tax liability. Tax planning is rarely an isolated activity but is usually carried out at the same time as financial and business planning.

In practice, tax planning for companies often involves:

- Reviewing how income is generated and recorded

- Understanding timing differences between revenue, expenses, and tax liabilities

- Considering how growth or restructuring may change obligations

- Ensuring compliance frameworks are still fit for purpose

None of this is especially dramatic. But over time, small misalignments compound. That’s usually when tax planning shifts from “background consideration” to urgent discussion.

Why Tax Planning Becomes Strategically Important

Businesses typically do not prioritize tax planning until its financial impact becomes visible. Taxes influence several core areas of business performance, including profitability, liquidity, and financial stability.

Tax planning becomes important because it directly affects:

- Net income and profit margins

- Cash flow forecasting and liquidity management

- Financial reporting accuracy

- Regulatory compliance and audit readiness

- Investor confidence and governance credibility

Unexpected tax liabilities can disrupt financial planning and place pressure on operational cash flow. In contrast, predictable tax obligations support more reliable forecasting and financial control.

In recent years, tax transparency and regulatory scrutiny have also increased globally. As a result, businesses increasingly view tax planning as part of broader financial governance rather than a narrow technical exercise.

When Tax Planning Becomes Relevant for Businesses

Interestingly enough, many firms don’t consider much tax planning until a specific event happens.

Common Triggers Include:

- Rapid growth or expansion into new markets

- Changes in ownership or group structure

- Increased profitability after years of modest margins

- Preparing for investment, audit, or exit conversations

It is during these times that the issue of managing tax liabilities becomes clear. The numbers that were previously manageable now become important. And the decisions made several years ago now have implications. Long-term tax planning, in this case, sometimes becomes clear when it is needed.

Common Tax Planning Approaches Used by Businesses

Although every organization is different, most businesses adopt one of several common approaches to tax planning.

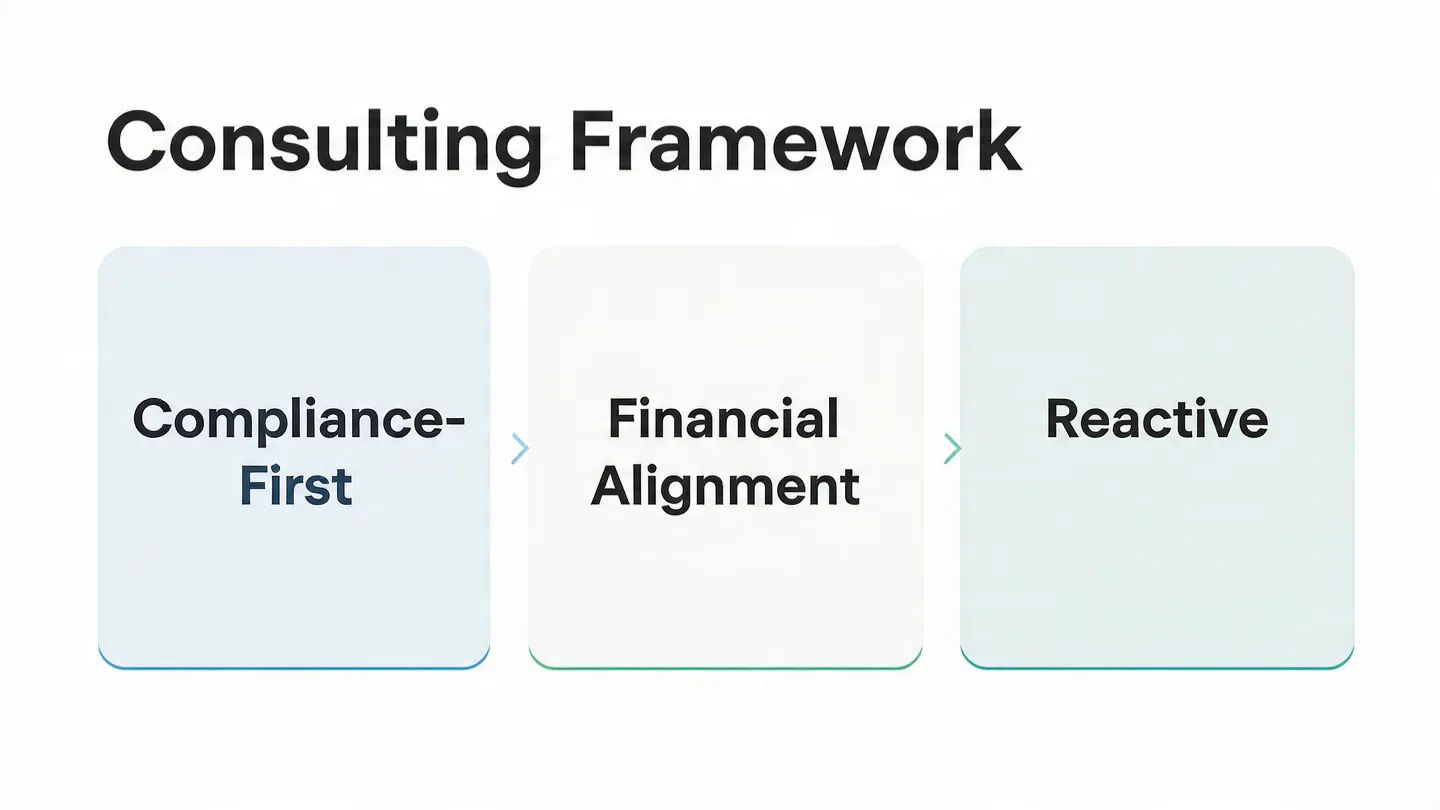

1. Compliance-Focused Tax Planning

This is the most widely applied method, particularly for existing and professionally managed businesses.

The main areas of focus include:

- Compliance with tax laws accurately and timely

- Accurate maintenance of documents and financial information

- Minimizing audit and regulatory risks

- Ensuring tax returns and financial information match

This method focuses more on stability, security, and regulatory compliance than tax minimization. For a large number of businesses, this is the best guarantee for long-term financial and operational security.

2. Integration With Financial Planning and Forecasting

More mature organizations integrate tax planning into their broader financial management processes.

This may include:

- Aligning tax obligations with cash flow forecasts

- Evaluating how capital expenditures affect tax treatment

- Monitoring the tax impact of growth initiatives

- Considering tax timing within financial planning cycles

In this approach, taxes are treated as a predictable financial variable rather than an isolated compliance burden. This improves financial planning accuracy and reduces the likelihood of unexpected liabilities.

3. Reactive Tax Planning in Growth-Stage Businesses

For young or rapidly growing businesses, a reactive approach to tax planning is common.

Tax planning may be a focus of attention in the following situations:

- At financial year-end

- In preparation for audits

- After a significant increase in profitability

- In response to a request from a regulator or other authority

For founder-led businesses, operational priorities are often more important than financial structuring, and a reactive approach to tax planning is common, although as businesses develop, this may change to a more formal approach to tax planning.

Tax Planning vs Tax Avoidance: Where Businesses Draw the Line

One of the most common misconceptions is that there is a fine line between tax planning and avoidance.

When viewed through a business perspective, tax planning vs. tax avoidance appears to be defined with regards to certain intentions. Most businesses usually seek:

- Clear commercial rationale

- Alignment with Actual Operations

- Positions that can be explained without discomfort

In theory, tough structures can mean tax savings. In practice, this may mean increased legal, reputational, or other kinds of risk. Yet for many people, it is simply not worth it. Ultimately, over time, this has resulted in a more measured and pragmatic approach within these industries.

Common Challenges Businesses Encounter

Even with good intentions, tax planning isn’t simple. Several challenges appear again and again.

Complexity Grows Faster Than Expected

As businesses expand, tax complexity increases often faster than leadership anticipates. Multiple jurisdictions, indirect taxes, payroll obligations. It adds up quietly.

Over-Reliance on Past Assumptions

What worked when revenue was modest may not hold at scale. Businesses sometimes continue with outdated structures because “it’s always been done this way.”

Fragmented Decision-Making

Tax considerations may sit with finance, while operational decisions are made elsewhere. Without coordination, gaps emerge.

Misunderstanding Risk

Some organisations focus too narrowly on short-term savings without fully appreciating long-term exposure. This is a frequent theme in common mistakes in business tax planning.

What Businesses Often Overlook

From experience-based observation, businesses often overlook softer—but critical—elements of tax planning. Take documentation, for example. Not just having it, but having it make sense to someone external. Or governance. Clear decision trails. Consistency in treatment year over year.

Another ignored factor is timing. All things are not required to be optimized at once. Sometimes it’s best to just know when the tax matters will hit. These are not technical gaps; they are organisational ones.

The Role of Advisors in Business Tax Planning

The role of the tax advisor in business planning is poorly understood. The advisor does not decide. Neither does an advisor work miracles.

In practice, the businesses normally use advisors to:

- Sense-check assumptions

- Interpret evolving regulations

- Provide external perspective

- Help align tax with commercial reality

Good advisory relationships are never transactional, but ongoing. They grow and develop as the business grows and develops. Importantly, advisory support doesn’t replace internal judgment; it completes it.

How This Connects to Advisory and CFO Services

From an advisory perspective, tax planning will be rarely treated in isolation, but rather as part of cash flow management, forecasting, governance, and compliance.

CFO and advisory services are helpful in giving the context within which tax planning is sensible:

- Understanding the complete financial picture

- Tax considerations aligned with growth plans

- Ensuring that decisions are defensible and documented

This is not about selling outcomes; it’s about creating clarity where complexity exists

Conclusion: A Thoughtful, Long-Term View

How do businesses plan their taxes? “Usually with caution. Sometimes imperfectly. Often incrementally.”

Most organizations take a balanced approach to tax planning, an exercise in trade-offs between efficiency and risk, flexibility and discipline, and growth and control. The best solutions are those that are careful rather than aggressive, integrated rather than isolated.

Understanding how businesses generally approach tax planning can involve many different things, but what it’s really not about is aping, or mimicking, what they do. It’s not about recognizing patterns, or difficulties, or trade-offs. It’s not even about deciding, carefully, how tax plays a part

Frequently Asked Questions

If you’d like to explore how tax considerations fit into a broader advisory or CFO-led perspective, you can learn more about our advisory approach or start a discussion with IQ Insight Consulting.